")

- mediflows

- billing cost

- June 1, 2026

- No Comments

Blog Details

Medical Billing Services for Physicians: Complete 2026 Guide

Plenty of practices outsource their billing for the wrong reasons and still come out fine. A smaller number do it for reasons that sounded right at the time and end up regretting it. What nearly everyone gets wrong is the first question they ask, which is “how much does it cost.” That’s the wrong place to start.

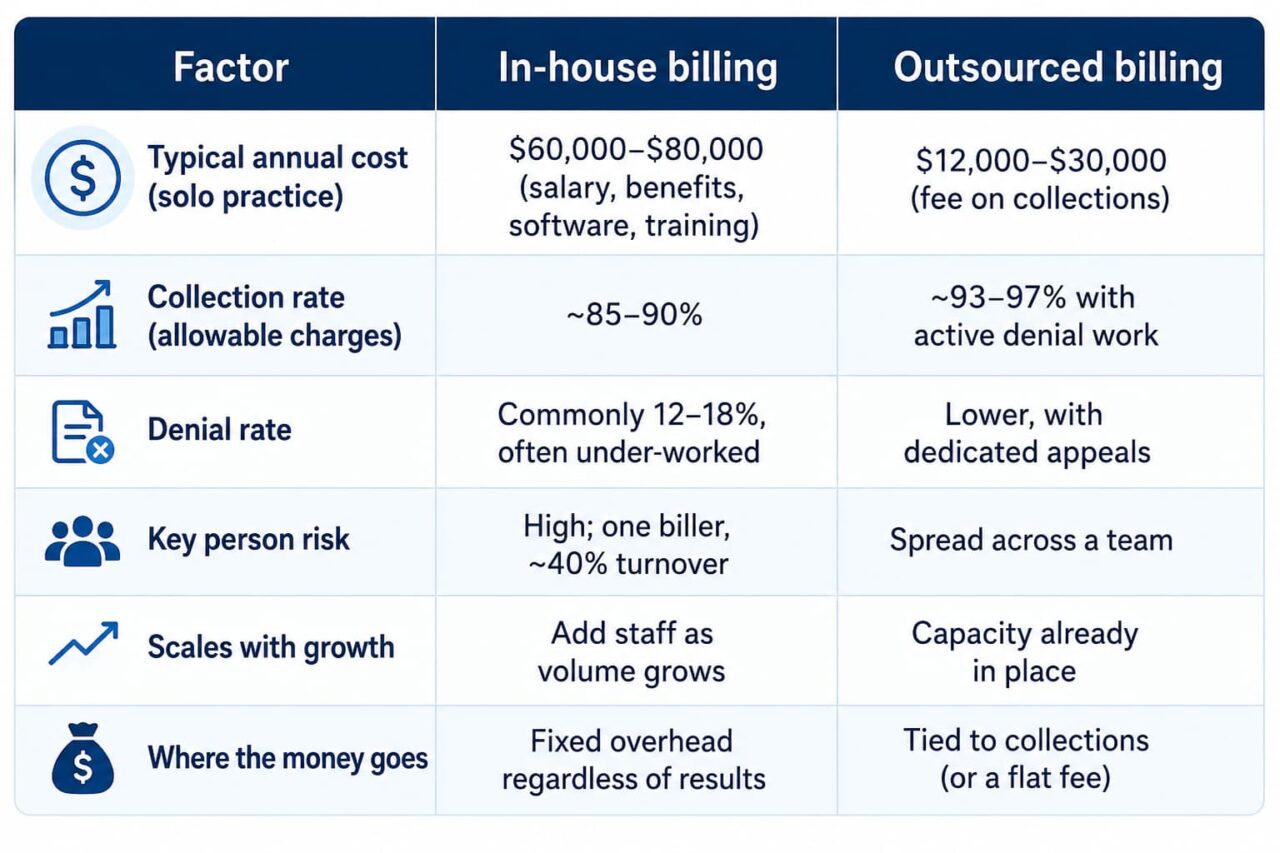

Start here instead. The average in-house billing operation collects somewhere around 85 to 90 percent of what a practice is actually owed. A billing team with real denial-management muscle tends to land at 93 to 97 percent. On a practice expecting $80,000 a month in allowable charges, the difference between collecting 88 percent and 95 percent is about $5,600 a month. That is roughly $67,000 a year you are either collecting or quietly writing off. The billing fee, whatever it turns out to be, is almost always smaller than that gap.

So the real decision is not “should I outsource.” For most small practices, the MGMA reported in 2025 that nearly 60 percent of groups under ten physicians are already weighing it. The real decision is whether you will outsource well or badly. This guide is the honest version: what these services do, what they actually cost, the pricing model that punishes you for growing, the fees buried in “simple” contracts, when you should not outsource, what to keep in-house, the questions that separate a good biller from a brochure, and how to switch without watching your accounts receivable collapse for three months.

What "outsource medical billing services" actually means

Outsourcing medical billing means handing the back end of your revenue cycle to a third party instead of running it with your own staff. The provider still sees the patient and documents the visit. After that, an outside team takes over: charge capture and coding review, claim scrubbing and submission, payment posting, denial work and appeals, accounts receivable follow-up, and usually patient statements and balance collection.

What it does not automatically include is everything. Some practices hand off the full cycle. Others keep the front desk pieces, like real-time eligibility checks and charge entry, and outsource only the claim-to-payment back end. Both are valid. The trouble starts when you assume “full service” covers a task it doesn’t, and you find out during a denial spike that nobody owns it.

A clear scope is the whole game. Before you compare prices, write down which of these you expect the vendor to own: eligibility verification, prior authorizations, coding, claim submission, denial management, AR follow-up, patient billing, credentialing, and reporting. Then make them confirm each one in writing.

The math that actually decides it

The cost question has a simple answer and a useful answer. The simple answer: in 2026, most outsourced billing runs 4 to 10 percent of collections, with the majority of practices landing between 5 and 8 percent. Complex specialties and very small practices sit higher, sometimes 10 to 12. On a per-claim model you’ll see roughly $2 to $12 per claim, and flat monthly arrangements tend to run from about $1,000 to $5,000 and up depending on volume.

The useful answer ignores the fee at first and looks at collections. Compare what you keep, not what you pay.

A solo practice running billing in-house carries a biller’s salary (commonly $55,000 to $75,000 in 2026), plus 20 to 30 percent on top for benefits and payroll taxes, plus software, clearinghouse fees, and training. All in, that’s frequently $60,000 to $80,000 a year for one practice. Turnover makes it worse; biller turnover near 40 percent means you periodically lose your only person who knows your payer quirks, and AR sits while you rehire.

Now layer in the collections gap. If outsourcing moves you from collecting 88 percent of allowable charges to 95 percent, the extra revenue usually dwarfs the fee. That is the calculation. A practice collecting $176,000 a month in-house at 88 percent versus $190,000 at 95 percent has found $14,000 a month, and a 6 percent fee on $190,000 is $11,400. Even in that example you net ahead, and you stop carrying the in-house overhead entirely.

This is also why the cheapest quote is rarely the cheapest deal. A 5 percent biller running a 78 percent clean-claim rate costs you far more than an 8 percent biller hitting 97 percent. Practices fixate on the percentage on the invoice. What actually keeps the lights on is the collection rate sitting behind it.

Here’s the same decision laid out side by side:

The table makes the trap visible. In-house looks like a controllable fixed cost, but the hidden line is the collection rate, and a few percentage points there outweigh almost any fee difference.

The pricing model that costs you more as you grow

Percentage of collections is the default, and vendors will tell you it “aligns incentives.” It does, partly. The biller earns more when you collect more, so there’s a reason to chase the hard claims. Fair enough.

Here is the part the sales pages skip. A percentage scales with your revenue, not with the biller’s effort. The work to submit and follow a clean claim is roughly the same whether you billed $80,000 or $180,000 this month, but a percentage fee on your collections more than doubles over that range. You grow, you add a provider, your volume climbs, and your billing cost climbs in lockstep even though the vendor isn’t doing proportionally more. Three good years and you can be paying for a luxury you’ve outgrown.

That’s the case for a flat or transparent fee structure, which is the model Mediflows is built around. A predictable fee means your billing cost is tied to the work, not skimmed off your growth. When you sign a new payer contract or add a provider and your collections jump, the savings stay with the practice instead of inflating the invoice.

Per-claim pricing has its own quirk: the biller earns the same on a $45 blood draw as on a $4,000 surgical claim, which can mean less attention on your highest-value claims. None of these models is automatically right. But you should choose with the trade-off in front of you, not because a vendor told you their model is the “aligned” one.

The fees buried in "simple" contracts

A headline rate is not a price. The number that matters is everything you’ll actually be charged, and the standard contract has more lines than the quote.

Watch for claim resubmission fees ($2 to $5 each, which adds up fast if their first-pass rate is weak), payer enrollment fees ($50 to $200 per enrollment), patient statement fees ($0.50 to $2 per statement), monthly minimums ($200 to $1,000 that you pay even in a slow month), early termination penalties (often three to six months of fees), and clearinghouse pass-through charges. Setup and implementation fees show up too.

Two of these deserve special suspicion. A monthly minimum punishes seasonal and growing practices, because you can end up paying well above your effective rate in any month collections dip. And an early termination penalty is the contract telling you it expects you might want to leave. A confident biller doesn’t need to lock you in for years. Ask for the fee schedule in full, in writing, before anything is signed, and add up the realistic annual total rather than the percentage.

When outsourcing is the right call, and when it isn't

Outsource when your denials are piling up faster than anyone can work them, when AR over 90 days keeps creeping up, when your one biller is a single point of failure, when you’re growing and billing can’t keep pace, or when you’re spending more on in-house billing overhead than the function is returning. In-house denial rates commonly sit at 12 to 18 percent, and each denied claim costs $25 to $100 in staff time to rework. If those denials are mostly going unworked, you are leaking money every week, and that’s the clearest signal of all. (Our hidden billing leaks breakdown covers where that money usually goes.)

Don’t outsource if your problem is actually a documentation or front-desk problem dressed up as a billing problem. A biller can’t fix charges that never get captured or eligibility that’s checked six weeks before the visit. If your providers aren’t closing encounters or your front desk isn’t verifying coverage, outsourcing the back end just moves the bottleneck. Fix the front end first, or hand that off too, deliberately.

Also think twice if you’re chasing the lowest rate above all else. A cheap biller who underperforms on collections is the most expensive mistake on this list.

What to hand off, and what to keep

Even after you outsource, you usually still carry some of the cycle, and the practices that get burned are the ones who assumed otherwise. Front-end eligibility verification, prior authorizations, and charge entry often stay partly in your office unless you explicitly contract them out. If you keep them, staff them. If you hand them off, confirm the vendor owns them in writing.

The cleanest setup makes one party accountable for each step end to end. Charge capture and coding through medical coding, real-time eligibility verification, claim submission to your payers, denial management and appeals, and AR follow-up should each have a clear owner. Gray zones between your team and the vendor are where claims die. If you also add a provider or open a location, credentialing and enrollment needs an owner too, because every month a new provider isn’t enrolled is a month of billable work you can’t bill.

How to vet a billing partner

Reviews and a US-based team are table stakes. The questions that actually predict performance are operational, and a good biller answers them with numbers.

Ask what clean claim rate, net collection rate, denial rate, and days in AR they hold for practices your size, and ask to see it. A vendor who reports on “gross billed” instead of net collections is hiding behind a flattering number; gross billed includes money you’ll never see. Ask whether you get a live dashboard or a PDF that arrives on the fifth of the month telling you nothing useful. Ask how denials are worked, by whom, and how fast, because that one workflow is where most of your recovered revenue lives. Ask for two references at practices in your specialty and actually call them.

Confirm the boring compliance pieces in writing. A signed Business Associate Agreement is not optional under HIPAA, and where the team sits, who can see protected health information, and what their breach protocol is should all be answered plainly. A partner that’s genuinely a fit for your specialty will have specific answers, not reassurances.

Switching without an AR cliff

The fastest way to ruin a good outsourcing decision is to rush the handoff. Claims in flight, payer enrollments, EHR and clearinghouse access, and open AR all have to move without a gap, and timely filing deadlines don’t pause while you transition.

Run the old and new processes in parallel for a stretch rather than flipping a switch. Map every open claim before cutover, agree on who works the legacy AR, and confirm payer enrollments and electronic remittance routing are in place before the new team submits a single claim. Expect a short dip while the new team learns your payer mix, and plan cash flow for it. Handled carefully, a switch protects your revenue. The practices that end up with 90 days of stalled collections almost always rushed it, then blamed outsourcing for a problem the calendar caused. Our pillar guide on medical billing for small practices lays out a week-by-week transition playbook if you want the detailed version.

One 2026 wrinkle worth naming: CMS adjusted the Physician Fee Schedule this year, and the

efficiency changes to work RVUs make coding accuracy matter more for profitability, not less.

With high-deductible plans now covering well over half of employer-insured patients (KFF,

2025), patient balances are a bigger slice of your revenue than they used to be, so a biller’s

patient-collection ability is now as important as their payer work. Whoever you hand the cycle to

needs to be good at both.

FAQ

Is outsourcing medical billing worth it for a small practice?

In 2026, most practices pay 4 to 10 percent of collections, with 5 to 8 percent being typical. Per-claim pricing runs about $2 to $12 per claim, and flat monthly fees range from roughly $1,000 to $5,000 and up. A solo practice that spends $60,000 to $80,000 a year running billing in-house often pays $12,000 to $30,000 outsourced, before counting the collections it recovers.

Should a small practice handle denial management in-house or outsource it?

For most, yes. The deciding factor isn't the fee, it's the collection rate. Moving from collecting roughly 88 percent of allowable charges to 95 percent usually recovers more revenue than the entire billing fee costs, and it removes the salary, benefits, and turnover risk of an in-house biller.

What percentage do medical billing companies charge?

Between 4 and 10 percent of collections, most commonly 5 to 8. High-complexity specialties and very small practices can run 10 to 12. Watch for what's excluded at the lowest rates; a 3 percent quote that leaves out denial management and patient collections isn't really 3 percent.

Categories

Tag Cloud